If you’re an Ontario homeowner looking to boost your cash flow and get ahead financially in 2026, consolidating debt on your mortgage could be your smartest move. High-interest credit cards, personal loans, and other debts can drain your budget, but by refinancing your mortgage, you can roll those balances into one lower monthly payment.

In this guide, we’ll walk you through exactly how to consolidate debt on your mortgage in Ontario, access your home equity, and take control of your finances, all while avoiding the common mistakes that can trip up borrowers.

Why Consolidating Debt on Your Mortgage in Ontario Makes Sense in 2026?

In today’s economic climate, interest rates on credit cards and personal loans often soar well above 18–20%, while mortgage rates remain significantly lower. For Ontario homeowners, consolidating debt on your mortgage is a smart way to lower your overall interest costs, simplify your finances, and boost your monthly cash flow. By using a mortgage refinance to consolidate debt, you can

- Lower your overall interest rate

- Reduce your total monthly payments

- Simplify your finances with one easy payment

- Improve your monthly cash flow

- Free up money for savings, investments, or emergency funds.

How Mortgage Refinancing Works for Debt Consolidation?

Mortgage refinancing is the process of replacing your current mortgage with a new one—usually to access the equity you’ve built in your home. When you consolidate debt on your mortgage, it allows you to roll high-interest debts like credit cards, loans, and other obligations into your mortgage. This creates a single, more manageable monthly payment at a lower interest rate, helping you regain control of your finances and boost monthly cash flow.

✅ Tip: Work with a mortgage broker who can shop around for the best refinancing options, not just stick with your current lender.

Why Mortgage Refinancing Makes Sense in 2026:

Interest Rates Are Stabilizing:

After several unpredictable years, the lending environment is becoming more stable. In 2026, refinancing offers homeowners an opportunity to secure better interest rates and improved loan terms.

Home Equity is still a thing:

Ontario’s real estate market continues to show resilience. As a result, many homeowners have built up significant equity in their properties, equity that can now be strategically accessed through refinancing.

Debt Has Become a Burden:

With the rising cost of living, more Canadians are relying on credit to make ends meet. Refinancing to consolidate high-interest debt into a lower-rate mortgage is not only practical… it’s financially smart.

Common Debts That Can Be Consolidated:

- Credit card balances

- Second mortgages

- Personal loans

- Auto loans

- Lines of credit

- Payday loans

The Refinancing Process: Step-by-Step

1- Review Your Current Debt.

- List balances, interest rates, and payments

2- Assess Home Equity

- Determine available Home equity. Typically, this is, 80% of your home’s value minus your mortgage balance.

3- Speak with a Mortgage Broker

- Get a customized refinancing plan.

4- Apply and Get Approved

- Submit documents.

5- Consolidate and Close

- Use new mortgage funds to pay off debts

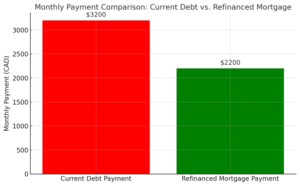

Real-Life Example: Meet Natasha from Mississauga

Natasha, a teacher from Mississauga, had $45,000 in combined debt (credit cards and car loan) and was paying over $1,100/month in interest-heavy payments.

She refinanced her mortgage to consolidate her debt on her mortgage using $60,000 of home equity. Her monthly payment dropped to $385, saving her over $700/month, giving her peace of mind and financial breathing room.

📉 How Consolidating Debt on Your Mortgage Impacts Your Credit Score:

Many homeowners worry that refinancing will hurt their credit score, and while it’s true that your credit may dip slightly at first due to a hard inquiry, the long-term impact is often positive. By consolidating multiple high-interest debts into a single lower-interest mortgage payment, you reduce your credit utilization and make on-time payments easier.

Even better, from the credit bureau’s perspective, it looks like you paid off all your debts in full, as if you had the cash to do it. This can significantly improve your credit score over time. Lenders also tend to view mortgage debt more favorably than revolving credit, making you look stronger on paper for future borrowing.

Benefits of Consolidating Debt on Your Mortgage:

✅ Lower Monthly Payments

Combining debts can reduce your total monthly outflow significantly.

✅ One Simple Payment

No more juggling multiple bills and due dates.

✅ Lower Interest Rate

Mortgage rates are typically much lower than unsecured debt rates.

✅ Improved Credit Score

Paying off revolving credit can boost your credit score over time.

✅ Increased Cash Flow for Investments or Emergencies

Extra room in your budget gives you options to invest, save, or prepare for the unexpected.

Common Pitfalls to Avoid When Consolidating Debt through mortgage refinance:

❌ Extending Your Term Too Much

Yes, a lower payment feels good, but be sure to make it worthy by paying your mortgage faster.

❌ Not Changing Spending Habits

Consolidation won’t help if you rack up new debt. Have a budget and a plan to stay disciplined.

❌ Ignoring Fees

Watch for penalties, legal costs, and lender fees. A good mortgage broker will walk you through these so you can understand the implications and total savings!

When Is Consolidating Debt on Your Mortgage the Right Move?

Ask yourself the following questions:

Do I have more than $20,000 in high-interest debt?

Do I have 20%+ equity in my home?

Am I struggling to keep up with monthly payments?

Do I want to simplify my finances?

If you said “yes” to two or more, refinancing may be your best financial move in 2026.

How to Get Started:

1- Check your home value and mortgage balance

2- Review your debts and current interest rates

3- Book a consultation with a mortgage expert (like Us! 😉)

4- Explore your refinancing options

5- Even if you’re not ready to refinance now, having the knowledge and a clear plan can make a huge difference in the months ahead.

FAQs About Mortgage Refinancing:

Q: Can I consolidate debt if my credit score isn’t perfect?

Yes. The key point here is having enough equity in your home. A mortgage professional can guide you toward lenders who specialize in these situations.

Q: Can self-employed individuals refinance to consolidate debt?

A: Sure thing. Self-employed individuals are welcome to consider this option.

Q: How much equity do I need to consolidate debt on my mortgage?

A: Most lenders require at least 20% equity to refinance your home.

🏡 Final Thoughts: Consolidating debt through your mortgage could be the turning point for lower stress, higher cash flow, and true financial freedom in 2026.

Debt doesn’t have to define your future, not when you have the right strategy and support.

Ready to take control of your finances? Book a free consultation today by clicking here and let’s build a customized plan to consolidate your debt on your mortgage, your future self will thank you.